User-first opening: what this means for someone getting started

If you’re setting up your first digital line of credit, practical clarity matters more than marketing blur. This guide focuses on how DiDi’s pay-later option shows up in real use and the concrete requirements for paying in installments, referencing didi prestamos and how their consumer products are presented as didi credito options. Grounded in everyday urban experience — think Mexico City’s ride-hailing adoption and the sharp rise in contactless payments after the COVID-19 pandemic — the aim is to give you steps you can follow immediately: eligibility basics, repayment mechanics, and what to watch for with interest and fees.

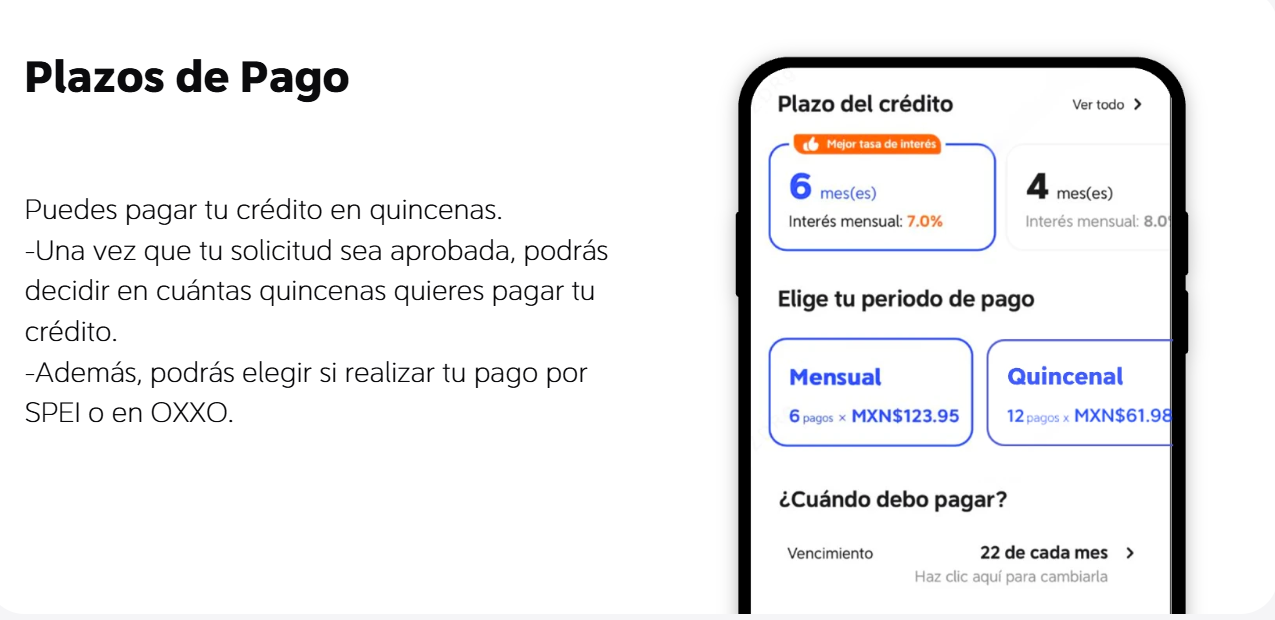

How DiDi Pay Later typically works for a new user

The service assigns a small credit line tied to your DiDi account that you can use at checkout or for rides, then repays it across set installments. Key components to expect: a soft credit check or internal scoring, a stated interest rate or APR, and an interface that shows due dates and outstanding balance. For many users the flow is simple: approval, use, and scheduled repayment — but that simplicity hides several product details you should verify before committing.

Essential requirements for approving and servicing installment payments

Most digital lines require a combination of identity verification, a linked payment method, and transactional history. Practically, that means submitting ID, connecting a bank card, and having recent activity on the platform. Lenders look at payment reliability more than just raw income, so regular ride or delivery activity can help. Industry terms to note include credit score, repayment schedule, and loan origination — these will appear in the terms and affect your APR and monthly installment amount.

What to check in the fine print — and common implementation pitfalls

Before accepting an offer, confirm the total cost over time, whether late fees compound, and how early repayments are handled. Many users miss merchant-level charges or minimum repayment thresholds — a costly oversight. Also verify whether the credit line is reusable after repayment or a single-use product. If you use this feature for daily expenses, keep an eye on the repayment cadence; mismatched pay dates and installments are the simplest way to slip into late fees. — A brief reminder worth repeating: automated convenience is useful, but it demands active tracking.

Alternatives and comparative insight

If DiDi’s pay-later product doesn’t fit, compare it with traditional credit cards, bank installment loans, and other fintech “buy now, pay later” services. Look at three dimensions: total cost (APR and fees), flexibility (early payoff and pause options), and integration (does the platform show your balance in-app and send timely reminders). In many urban markets, competition has driven clearer UI and embedded repayment tools, but features vary — always compare the experience and not just the headline rate.

Three golden rules for evaluating a digital line of credit (Advisory)

1) Confirm the real total cost: add fees, interest, and any origination charges to the principal to see the true monthly burden; only then compare options. 2) Match repayment cadence to your cash flow: choose a schedule with due dates that align with payroll or predictable income to avoid late charges. 3) Prefer transparent platforms: pick services that display outstanding balances, next due date, and year-to-date interest in the app or statements — this reduces surprises and helps budget accuracy.

Closing: how this delivers value in practice

Applying these rules will let you use DiDi’s pay-later features without guesswork and with a clear plan for installments; that clarity is what turns convenience into a useful financial tool. For many urban users, the blend of platform integration and straightforward repayment management is the real advantage — and the one you should expect when choosing a provider like DiDi Finanzas. —